39–Lever #3: Spending (Part Eight—Budgeting)

Foundational to wise financial stewardship

This is the last “Lever #3: Spending” series article. It is the one where we will bring it all together as a workable plan that helps you steward your financial resources in a way that prioritizes giving and creates margin so that you have something extra to save for the future and to respond to the unexpected.

This is important because if you want to give generously and get ahead financially (in other words, have a positive net worth), you must start with one major but often overlooked tool: a budget. When some people hear the dreaded “B” word, they freak out or get a little “twitchy.” It sounds restrictive, even suffocating, and overwhelming. (I’ll wait while you take a breath…) But a budget isn’t about restrictions; it’s about discipline that leads to freedom—freedom from stress and to spend, give generously, and save for future needs.

I know you remember our Financial Life Equation (though you may have hoped I’d forget it). Here’s a shorthand “plain english” version as a reminder:

Future Wealth = Starting Wealth + ∑Income – ∑Taxes – ∑Giving – ∑Expenses + ∑Interest Earned – ∑Interest Paid

Now, think about a budget and all its parts, and you will quickly realize that as a day-to-day cash management tool, it impacts nearly every variable in that equation. In that sense, it is one of the most impactful levers you can pull. “How so?” you may ask. Well, here’s a table to help you see how important a budget is to your current and future financial health in literally every category:

Despite these benefits, many people lack a budget. Instead, they operate under one of these "plans" (credit goes to Jaime Munson, Money: God’s Good Gift , a book I highly recommend, for these categories):

The Ignorance Is Bliss Plan: Check your balance at the ATM. If there's money, spend it! Never mind that there may be multiple transactions or bill payments you don’t consider when making that decision. Do the words “overdraft fees” ring a bell?

The Parent Bailout Plan: Call your mom or dad for a rescue when you run out of money. Sure, they are understanding, kind, and generous, but they are also quietly wondering (and hoping for) when you will stand on your own two feet financially.

The Credit Card Plan: Spend now, pay later (hopefully). Can’t pay? Just open a new card when the old one maxes out—paying credit card payments with a credit card. (Yes, it happens—a lot!)

The Hand-to-Mouth Plan: Spend everything you earn monthly—no cushion, no plan, just survival. This is the “no money left behind” spending plan. If this is you, I would encourage you to go back and reread the previous articles in this series, especially the ones about the need for margin and spending less than you earn.

Which of these “plans” (which are not really plans at all) are you using? Well, only one plan truly works: a reasonable spending plan—a/k/a a budget—based on a strategy that honors God, builds your financial future, and gives you freedom, flexibility, and peace.

You may wonder, “How do I develop this so-called wonderful spending plan?”. Well, I’m glad you asked. But before I answer, I need to say from the start that there is no “one-size-fits-all” here, but there is one that is right for you. I often suggest that you do SOMETHING, which is probably different than what you are doing and certainly something other than the plans that Munson listed.

Let’s walk through how to build that kind of plan. The basics of budgeting are simple: Know what you have coming in and where it's going. (I jokingly refer to this using the technical accounting terms: ”goesintas and goesoutas”.) If you don't have any kind of budget yet, take five minutes; grab a piece of paper or your laptop, or open Notes on your phone, and start two simple lists:

1—Monthly Income: List all sources of income—your paycheck after taxes, any side gigs, and anything else that puts money into your hands or bank account. Be cautious when handling items such as yearly bonuses or lump-sum commissions, as their value can fluctuate from year to year.

2—Monthly Expenses: You may have to gather some statements and receipts for this part. A good way to start is to download the last 12 months of all bank and credit card statements; that will help ensure you catch more expense items that can be easily overlooked. You may want to import and sort them in a spreadsheet, organizing them in categories.

Start with the big, non-negotiables: rent or mortgage, groceries, car payments, utilities, insurance, and cell phone bills. Then, add smaller recurring costs, such as streaming subscriptions (you may be surprised), gym memberships, and routine shopping (including groceries, clothing, and household supplies). Do not forget irregular expenses (such as car insurance paid twice yearly); divide them into a monthly equivalent.

Next, subtract expenses from income and see what you come up with. You have seen this equation before.

If I > E, congratulations—you have a margin!

If your expenses exceed your income (I < E), you need to make changes fast; either cut costs or increase income. If you think you have an income problem, consider a side gig. Or maybe you need a job that pays more. Sit down, list your options, and decide (prayerfully) what makes the most sense for you.

If you need to put your focus on your expenses, look for ways to cut costs. Look at your expenses and see what looks “out of whack.” Is it your car, rent, or eating out? Too many trips to the coffee shop? Perhaps you’re paying a lot on debt.

If you are going to do something about I<E, you will have to get creative. But there are ways to make more and spend less. Pray and seek wisdom and guidance. I’ve also included some resources below.

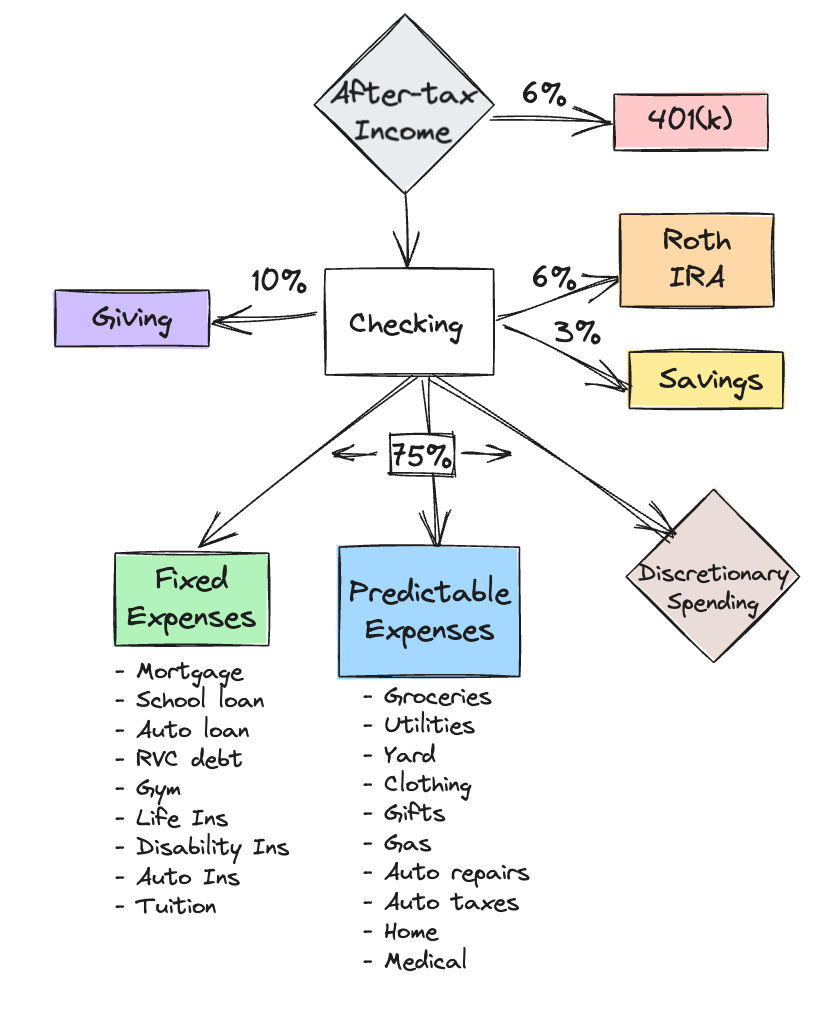

Once you know where you stand, you can start planning where your money should go. The graphic below is a helpful way to structure your budget based on six major categories: Giving, Long-Term Savings, Short-Term Savings, Fixed Expenses, Predictable (but variable) Expenses, and Discretionary Expenses. (I’ve included some common sub-categories under each one.) Thinking this way simplifies what can otherwise feel overwhelming.

I typically suggest you do your regular giving “off the top.” In the diagram, contributing to a 401(k) is the priority, but that’s because contributions are typically withheld from your pay along with other withholdings, such as taxes and insurance. Still, as you can see, giving and saving for short—and long-term needs are priorities.

I have included some suggested percentages in the example above, but that is all they are—suggestions. If your giving and total spending in all three major categories exceed 85% of your net income, you won’t have any surplus to save. That’s why using a budget is so important.

Let’s take a look at each major category:

1—Giving

I will repeat: I believe giving should be a top priority for Christian stewards. It reminds us that God owns everything and that our ultimate goal is to manage His resources for His glory (Psalm 24:1).

Giving can be divided into two categories. Some use the terms “tithes and offerings,” but you could use something like “firstfruits giving” and “spontaneous giving.”

Firstfruits giving would typically be to your church and perhaps other ministries you regularly support. Spontaneous giving involves helping someone in need, donating to worthwhile causes, or picking up the lunch tab when you are out with a friend.

Giving shapes your heart and your financial habits. So, build giving into your budget first, not as an afterthought; it is not the “leftovers” after you do numbers 2 through 6 below.

2—Emergency Savings

Saving is important because it helps you prepare for future needs and unexpected events. Set aside money for emergencies—ideally start with a basic fund of $1,000—and then build it up to 3 to 6 months of income as soon as possible.

The goal is to handle minor emergencies and build a cushion against job loss.

3—Long-Term Savings

As I’ve discussed before, if spending is necessary and giving is a priority, then saving is actually what’s left over. If you spend too much, you will have little or nothing to save.

The focus here is on retirement savings in tax-favored accounts such as 401(k)s and IRAs. However, saving for major purchases, such as a down payment on a house or opportunities that God may call you to pursue, is also essential.

Long-term saving also helps you plan for joyful events, such as weddings, mission trips, or a memorable vacation. God may ask you to give some of it away.

Saving for the long term is essential, but your priority should be filling up your short-term emergency savings bucket first. Yes, the sooner you can start saving for the long term, the better. But you’ve got plenty of time, and this sequence is vital for helping you stay out of debt, especially when the unexpected happens.

4—Fixed Expenses

These monthly expenses remain the same: rent, car payments, insurance premiums, and student loan payments.

You usually can’t change these easily or quickly, so they should be among the first things you account for after giving and saving.

Be cautious about taking on too many fixed expenses—over time, they can box you in and limit your flexibility. There is no hard rule here, but generally they should be between 35% and 45% of your total monthly expenses (refer to the above graphic). Once they get over 50%, you will be highly constrained in other areas.

5—Predictable (but Variable) Expenses

Predictable expenses are those that are necessary or likely to be incurred, but their amounts can vary, such as groceries, gas, electricity, and clothing.

Learning to control costs is a big key to mastering your budget. Meal planning, sharing rides, and shopping with a list are all small moves that add to significant savings.

The more you manage variable expenses, the more margin you can create for the things that matter most.

6—Discretionary Spending

Finally, there is discretionary spending, such as eating out, coffee runs, hobbies, and entertainment. Enjoying some discretionary spending is good—it reflects the goodness of God's creation and provision. But without guardrails, it can sabotage your bigger goals.

If E<I, and you don’t have an emergency fund, this is where to cut first. Then see where you can reduce your variable expenses. Brainstorm to devise a list of ideas, go with the most feasible ones, and tackle the more challenging ones down the road.

A budget helps you enjoy fun spending without guilt because you know it fits within your larger stewardship plan.

I want to emphasize again that there’s no one-size-fits-all method to budgeting. The best approach is the one you’ll stick with. Here are some popular options to help you get started:

The Zero-Based Budget: This is Dave Ramsey’s recommended approach, and it is a good one; however, it takes time to develop. Every dollar has a job. You plan your entire monthly income down to the last penny, assigning it to the different categories and sub-categories I showed earlier.

Pros: Maximum control. Great for those serious about building financial discipline.

Cons: Requires regular tracking and adjustments.

Recommended tool: Try Ramsey Solutions’ EveryDollar app for an easy-to-use, zero-based budgeting tool.

The 60/20/20 Budget: Split your income into simple percentages. You can adjust the percentages for your situation, but keep saving and giving as non-negotiables.

60% for needs (rent, utilities, groceries)

20% for wants (entertainment, travel, hobbies)

20% for savings and giving

Pros: Simple to implement and understand.

Cons: You may need to adjust if your "needs" exceed 50%.

The Envelope System: Dave Ramsey recommends this approach for individuals just starting to eliminate debt. You allocate cash for different categories, such as groceries, dining out, and clothing. Once the envelope is empty, stop spending in that area until next month.

Pros: Physically limits overspending. It makes money feel "real" again.

Cons: It can be awkward sometimes, and cash isn't practical for every expense in today’s digital world. However, there are digital envelope apps (see the discussion on tools below).

The "Pay Yourself First" Approach: Automate saving and giving as soon as your paycheck hits your account. Setting up automatic transfers to savings or investments makes this approach almost effortless. Whatever remains covers your living expenses.

Pros: Builds savings automatically and consistently.

Cons: Requires awareness of how much you have left for bills and discretionary expenses.

Budgeting tools can make all of this a lot easier. You don’t have to figure this all out manually. I was a long-time Quicken user, and more recently, I have used Banktivity for Mac, as I found Quicken’s product for Mac to be lacking in certain areas (and sub-par compared to its Windows version, which I had used for many years).

Here are some great tools and apps that can help you manage your budget better:

Experiment with different options to find what works best for you. Consistency is the key, not perfection.

When you live with a plan—spending intentionally, giving generously, saving wisely—you reflect the heart of a faithful steward. You free yourself to say "yes" to God’s opportunities without being chained to financial stress.

For reflection: What do you think about budgeting? Do you consider it a burdensome chore, something to be avoided? Or do you obsess over it, trying to figure out how to track every penny? As Christians, we can approach budgeting as a spiritual discipline, part of our discipleship. It's a tool we can use to help us wisely steward what God has entrusted to us.

Verse: “The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to poverty.” (Proverbs 21:5, ESV).

Resources:

Art Rainer, Find More Money: Increase Your Income to Tackle Debt, Save Wisely, and Live Generously (Nashville: B&H, 2020). (Note: Art is co-owner of Rainer Publishing, who graciously agreed to publish my second book, The Minister’s Retirement.)

Chris Guillebeau, The $100 Startup: Reinvent the Way You Make a Living, Do What You Love, and Create a New Future (New York: Crown Publishing, 2012).