19—Lever #1: Your Income (Part Seven—Transferring the Risk)

Handle what risk you can, transfer the rest

In the last article, we discussed risk and the various ways to deal with it. You have options, and probably the best way to deal with high-impact but low-probability risk events is to “transfer” it.

The first way to transfer risk and the concerns and perhaps the fears that come with them is to submit them to the Lord, "…casting all your anxieties on him, because he cares for you” (1 Peter 5:7b, ESV).

Okay, I admit I'm taking some liberty with the word "transfer" here; that's not actually how it works. "Humbly submit out of dependence and trust" would be better, but I think you get my drift.

Another way is to transfer some of the risk to an insurance company. That can also be very wise in certain situations, as it involves a literal transfer. However, transferring risk comes at a cost—you're betting you will lose money in the deal. How so, you ask?

Insurance is a contract between you and an insurance company that pays a benefit when something bad happens but pays nothing if you don't suffer a loss. You pay premiums, hoping you never need to receive the benefit of the insurance you purchased with them.

If that sounds like an unwise financial gambit—spending money on something we hope we never realize a benefit from—I understand. But here's the thing: a benefit is triggered when a qualifying event occurs; our insurance protects us from catastrophic losses. It doesn't prevent them altogether, but it reduces their effect.

Insurance is a critical part of a broader financial plan. It can help with a major illness or disability, provide replacement income after losing a spouse, and help repair or rebuild a home lost through a disaster.

Unfortunately, I don't know of any insurance that will protect you from losing your job; you'll need to "self-insure" with a 3- to 6-month emergency fund (larger, perhaps 12 to 18 months, if you are a family’s sole provider). (You could try to get an employment contract—good luck.)

Even though insurance can never cover every scenario, it can be a wise way to protect your income and assets. But if you're younger, your needs for insurance protection differ from those who are older. And married couples, especially those with children, have very different needs than young single adults.

Insurance is big business, but it's a relatively simple concept. Insurance companies collect premiums, assess their customers' risks, and then pool them together in "risk pools." Sounds pretty creepy, right?

These "risk pools" are groups of people sharing a common risk—such as accident, injury, or death—spread across the entire group or "pool." As a pool member, you pay money in (that's your premium). The insurance company invests it, usually in conservative fixed-income securities.

Money leaves the pool to pay those who suffer a loss from an "insured event" called a claim. (Coverage provisions determine what qualifies as an "insured event.")

The insurance company pockets the difference between the two, which is their profit. It pays out profits as dividends or retains them as reserves. If it operates at a net loss, reserves are drawn down, and premiums rise (or the insurance company goes out of business).

So. insurance is simply a pooling of risk regarding future events. It uses more complex and sophisticated forms of probability and statistical analysis (and actuarial science) than we discussed in the previous article.

Since risk is pooled, insuring oneself is not inherently gambling (although some insurance contracts can be). It is a common historical practice that goes back to biblical times (the Roman Empire provided life insurance for their soldiers).

There are many different kinds of insurance, but almost all of them involve paying a premium to an insurance company in exchange for coverage that can help cover your life, health, property, vehicles, and other things. (You can even buy meteor and asteroid insurance if you need it. I’m not sure you do unless you live on one of Jupiter’s moons.) The more extensive the coverage, the higher the premiums.

You can act as your own insurance company in some situations when self-insurance (i.e., assuming the risk) is obviously viable (for cell phones, extended TV and appliance warranties, and similar products).

You can also save on premiums by buying high-deductible insurance, but you need a cash buffer for that. You can profit from acting as your own insurance company, but only if you have few claims (and they are small).

Insurance has become more costly because the items it is meant to replace, if lost or damaged (such as homes and cars), have become more expensive. I'm unsure, but life insurance may be cheaper these days because people live longer. And it costs less when you are younger.

Like most people, I dislike spending money on insurance. As a retiree, I counted them up and have at least nine different insurance policies, including those related to Medicare.

Some Christians may question whether insurance is a biblical concept. Are we trusting in an insurance company rather than God? I'll give you my perspective, but there are others.

The Old Testament has much to say about using wisdom in this area. Insurance can be a way to provide for unforeseen circumstances in the future (Genesis 41). Proverbs speak to stewardship, particularly in the areas of preparation and saving for unexpected future events (Proverbs 24:23-27, 27:1, 27:12). I believe these principles can be applied to our perspective on insurance.

Ecclesiastes 11:1–2 also seems to have applicability here: “Cast your bread upon the waters, for you will find it after many days. Give a portion to seven, or even to eight, for you know not what disaster may happen on earth” (ESV).

The New Testament also speaks to this. 1 Timothy 5:8 says, “But if anyone does not provide for his relatives, and especially for members of his household, he has denied the faith and is worse than an unbeliever” (ESV).

Insurance can be a wise way to protect others and the assets and income God blesses you with. Still, whether insurance is the best option in any particular situation is ultimately a matter between you and God (James 1:5).

But we must be careful not to allow insurance to replace God. The goal of every protection plan should be to balance wise planning and faith in God, enough to protect you and your family, but not so much as to limit your dependence on God.

So, ultimately, whether to purchase certain types of insurance is a matter of personal conviction. The decision to buy or not to buy insurance must be made in faith. But remember that lenders require some insurance, and the government (auto, home, if you have a mortgage, etc.).

When you're younger and just starting out, you have a limited need for insurance. That changes significantly when you get married and when you start a family. Therefore, protecting and preserving present and future income streams is critical, especially if others depend on your income for their provision.

You can't risk self-insuring when you're young, "handling things as they come.” Sure, you may be able to absorb a minor setback with a decent-sized emergency fund, but a catastrophic event could wipe you out—"bye-bye savings."

Protecting your current and future income takes several forms.

First, protect your job (as much as you can). That means working for a reasonably stable company and not doing dumb things that get you fired.

In my experience, you have to do something terrible or do a lot of less bad things for a pretty long time to lose your job. Layoffs are different. They can happen randomly, and you can lose your job due to a reorganization or cost-reduction measures.

Do the words "downsizing" or "rightsizing" ring a bell? How about "flattening the organization," which is HR-speak for laying off a bunch of managers and doubling the size of the groups that those that remain have to manage?

I'll tell you a little secret: Companies and managers often use so-called "layoffs" to eliminate lower-performing employees. Not always, but that's frequently how individual displacement decisions are made as part of a more extensive layoff.

If you lose your job, you could end up with negative income (borrowing to make ends meet), which wreaks havoc on the Financial Life Equation, at least for a while. So do all you can to prevent that from happening. If it does, don't waste time feeling sorry for yourself; assume your new full-time job, which is looking for a new one. Ultimately, you can only do so much here, as employers and companies are unpredictable (and sometimes irrational). Just do what you can.

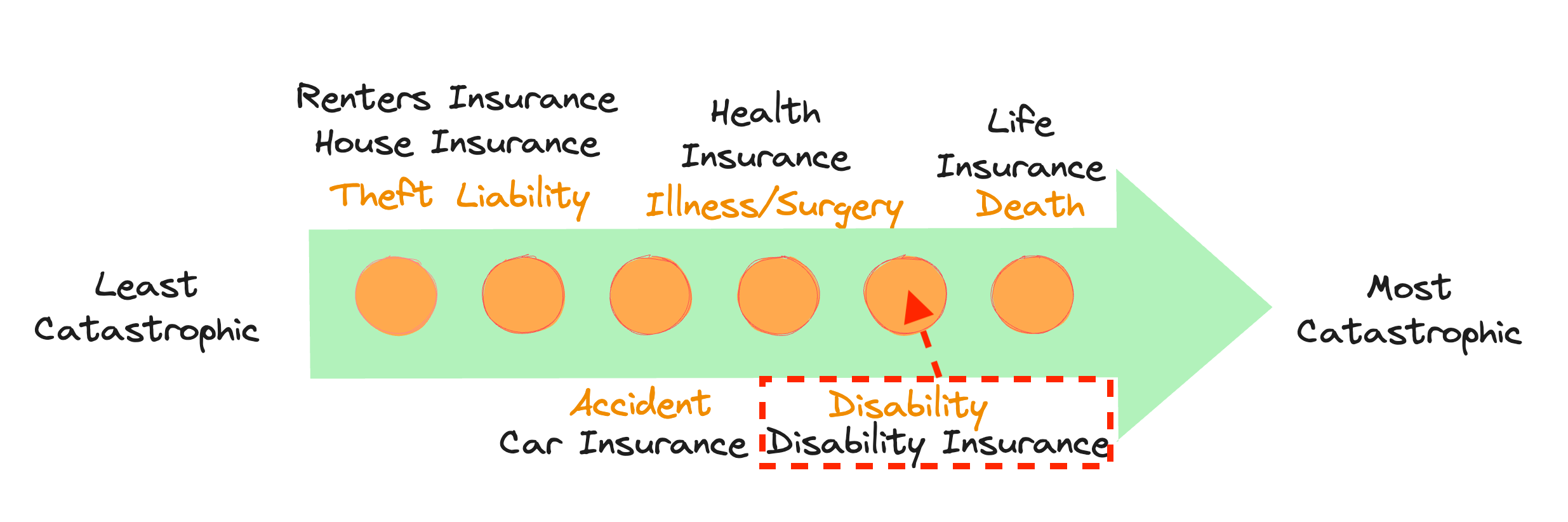

Second, you also need to protect against the effects of a debilitating illness or accidental injury resulting in short- or long-term disability, which makes it impossible for you to work and earn a living. A long-term disability early in life can have devastating consequences because of its impact on your future earning (and saving) potential. Therefore, having long-term disability coverage is usually wise (and it tends to be inexpensive when you're young).

Here's our "risk continuum" again. Job loss isn't on it because you can't actually buy insurance for that, even if you're self-employed. Notice that disability (especially long-term) is toward the "high risk" end:

Many employers provide short-term disability coverage at little or no cost. These policies usually replace between 40% to 70% of your salary for several months.

Long-term benefits are less common because coverage is more expensive than short-term. If you get it through your employer, short-term disability coverage may be available immediately; long-term coverage may be available after some years of employment. If so, consider enrolling in it. If not, consider outside insurers (although this may result in a slightly higher cost since you're not part of a group plan).

Finally, protect your income-producing (and growing) potential. You do that by doing all you can to maintain and improve your job skills through education and training. When it makes sense, pursue promotions, new jobs, or career opportunities.

Some final thoughts:

Insurance purchase decisions must be made carefully. I am reminded of this sales pitch from a life insurance salesperson to a hesitating customer: "Don't let me frighten you into a hasty decision. Sleep on it tonight. If you wake in the morning, call me then and let me know." Ha ha.

Seriously, take your time, research, and sleep on it if necessary.

Think twice about filing that insurance claim. Very often, when you file a claim, such as for an automobile accident or house damage, your insurance premiums (or your parents’ if you’re on their policy) will increase. And sometimes your policy will be canceled—yes, insurance companies can do that.

How much your premiums will increase depends on your policy and the claim amount. If you have a high deductible and cover it that way, you’re okay (unless you were charged with the accident, which can affect your premiums no matter what).

If you can afford it, consider paying the cost of the claim if your premiums are likely to increase. Do the math to determine your “breakeven” period and see if that makes sense.

Any changes to your premium must be made at renewal, even if you had an accident, filed a claim, or got a ticket in the middle of the term.

Your insurance company can decide to cancel your policy (or “non-renew”) for almost any reason when it comes up for renewal at the end of the policy term. Typically, your claims have been too numerous or significant for you to be a “profitable” customer.

Required notice will vary by state, but your insurer must give you written notice of cancellation or nonrenewal and the reason why. North Carolina, for example, requires a 60-day notice. You can appeal if you believe the cancellation is based on inaccurate information.

We haven't discussed two biggies in detail: protecting your health and life. I hate to state the obvious, but you can't earn a living if you're sick or injured or if you've gone to heaven (although you may not need to at that point, your family will still need one). We'll look at these more closely in the following couple of articles.

For reflection: Protecting your ability to generate a lifetime of income is one of the most important things you can do. Have you thought of insurance that way or viewed it as just a necessary expense without giving it much thought? What’s your view of God’s sovereignty, his providential care, and buying insurance? In what ways, if any, does it differ from the perspective shared in this article?

Verse: “The prudent sees danger and hides himself, but the simple go on and suffer for it” (Proverbs 27:12, ESV).